In both the private and public markets, valuations for B2B software companies continue to climb. The average publicly traded cloud company trades at nearly 12x forward revenue, while in the private markets, investors are considerably more aggressive. With record levels of private capital, continued outperformance in the public markets and a zero interest rate environment, it can be hard to imagine an impetus for slowing down this runaway software train (even the COVID-19 pandemic has not yet been successful!).

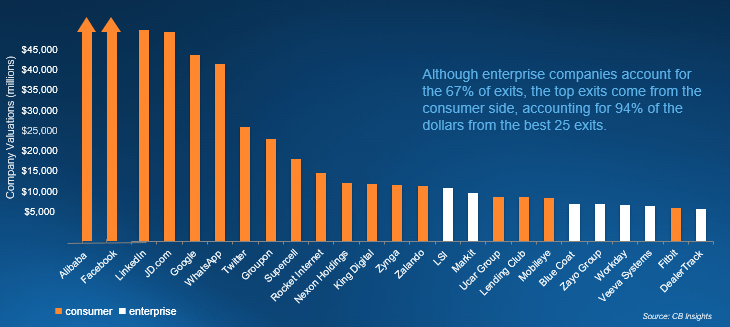

Yet, only four or five years ago, outsized exits in the enterprise sector were outliers. In 2016, we built the slide below (showing value at the time of IPO/acquisition) to demonstrate the dominance of large B2C exits. Back then, the 14 most significant venture-capital outcomes came from consumer companies, and the first enterprise outcome listed was LSI, a semiconductor company acquired for $6.5B in 2014.

Image Credits: Menlo Ventures/CB Insights

Times have changed. In 2019 alone, seven enterprise exits would make this chart (Slack, Qualtrics, Datadog, CrowdStrike, Cloudflare, 10x Genomics and Zoom). As I write this, 14 enterprise software businesses boast a market cap exceeding $20B.

To further illustrate this point, the two most valuable private venture-backed businesses (Stripe and SpaceX) are both enterprise businesses, and the top 25 most valuable companies are now nearly evenly split between consumer and enterprise. If this truly reflects the pipeline for the next generation of significant VC exits, we should expect the pendulum to continue to swing in favor of enterprise investing.

Recent Comments